What Is Equity Compensation Explained

Equity compensation is a powerful way for companies to pay you beyond a traditional salary. Instead of just cash, you get ownership in the company you work for. This means you receive a direct stake in the business's future success.

Understanding Your Stake in the Company

At its heart, equity compensation means you own a small piece of the pie. Think of yourself less as an employee and more as a partner in a growing venture. If the company does well and its value increases, so does the value of your piece. It's a common strategy, especially in the startup and tech worlds, to bring in top talent when cash for big salaries might be tight.

This completely changes the dynamic of your job. You're not just there to collect a paycheck; you're invested in the long-term vision. This creates a powerful shared incentive—everyone is pulling in the same direction because the company's success translates directly into personal financial gain.

More Than Just a Paycheck

Equity is a huge part of your financial life, but it’s meant to work alongside your salary, not replace it. To see the full picture of what you're earning, you need to understand how all the parts of your offer work together. It’s worth taking a moment to explore what a total compensation package includes to see how equity fits in.

Your salary is your predictable income for day-to-day life. Equity, on the other hand, is all about the potential for significant long-term wealth. It’s a trade-off: guaranteed money now versus a possibly much larger—but less certain—payout down the road. For marketers, getting this balance right is crucial when weighing an offer from a stable corporation against one from a high-growth startup.

The real power of equity is that it turns employees into stakeholders. When your financial success is directly tied to the company's performance, your perspective shifts from short-term tasks to long-term value creation.

The Basic Forms of Equity Ownership

Companies hand out ownership in a few different ways, and each comes with its own set of rules and perks. We’ll get into the nitty-gritty later, but it helps to start with a quick overview of what you're likely to see.

Here's a quick rundown to get you started.

A Quick Look at Common Equity Types

This table summarizes the main forms of equity compensation, giving you a high-level view of what each one is and its primary benefit.

| Equity Type | What It Is in Simple Terms | Why It Matters to You |

|---|---|---|

| Stock Options | The right to buy company stock at a fixed price in the future. | Lets you cash in on the stock's growth without having to buy shares right away. |

| RSUs | A promise to give you company shares once you've worked there for a certain time. | You get the full value of the shares without paying anything for them. |

| ESPPs | A program letting you buy company stock, usually at a discount, through payroll deductions. | An easy, often discounted, way to build ownership in a public company. |

Each of these is a different path to becoming an owner. Getting a handle on the basics is the first step to making sense of your offer letter and asking the smart questions. Think of this as your starting point for figuring out how these tools work and what they can mean for your career and finances.

The Different Ways You Can Own Equity

Equity compensation isn't a one-size-fits-all deal. It comes in a few different flavors, and each one has its own set of rules, perks, and potential pitfalls. Getting a handle on the differences is the first step to figuring out what your offer is truly worth. Think of it like learning the rules to different card games—they all use a deck of cards (the company stock), but how you play your hand to win is completely different for each one.

We'll walk through the most common types of equity you're likely to see: Stock Options, Restricted Stock Units (RSUs), and Employee Stock Purchase Plans (ESPPs). Once you understand how they work, you'll be in a much better position to evaluate job offers and map out your financial future.

This concept map helps visualize how equity ties together your salary, your sense of ownership, and the company's growth potential.

As you can see, equity is the bridge that turns you from a salaried employee into a stakeholder—someone with a real, vested interest in where the company is headed.

Stock Options: The Right to Buy Shares

Stock options are a classic, especially in the startup and tech scenes. An option isn't actually a share of stock. Instead, it’s the right to buy a set number of shares at a fixed price sometime down the road.

That locked-in price is called the strike price or exercise price. The whole game is based on the hope that when you decide to buy (or "exercise") your options, the stock's actual market value will have soared far above your strike price.

Here's an analogy: Imagine being given a coupon that lets you buy a designer handbag for $100. Right now, the bag sells for $100, so the coupon doesn't do you much good. But what if, in two years, that bag becomes a hot commodity and is selling for $1,000? Your coupon is now pure gold. You can still buy the bag for $100, giving you an instant $900 paper profit. Stock options work the exact same way. All the value is in the gap between your strike price and the future market price.

You’ll generally run into two types of stock options:

- Incentive Stock Options (ISOs): These are often the employee favorite because they can come with some nice tax advantages. If you hang onto the stock for a certain period after exercising, your profits might be taxed at the lower long-term capital gains rate, not as regular income.

- Non-Qualified Stock Options (NSOs): These are more common and give companies more flexibility. The catch for employees is that the profit—the difference between the strike price and the market value when you exercise—is taxed as ordinary income, which is usually a higher rate.

Restricted Stock Units: The Promise of Shares

Restricted Stock Units, or RSUs, work very differently. Instead of giving you the right to buy stock, an RSU is a straight-up promise to give you shares later, as long as you meet a condition. That condition is almost always just staying with the company for a certain amount of time.

Once your RSUs vest, the shares are yours. They just show up in your account. You don't pay a strike price to get them. Their value is simply the market value of the stock on the day they land in your possession.

If stock options are like a valuable coupon, RSUs are more like a gift card that unlocks over time. You don't pay anything to get the value; you just need to stick around long enough for it to become available.

This makes RSUs a much less risky form of equity. With options, if the stock price sinks below your strike price, your options become "underwater" and are essentially worthless. But with RSUs, as long as the stock has any value at all, you get something. For instance, if you're granted RSUs when the stock is at $50 and it drops to $20 when you vest, you still get shares worth $20 each. In that same scenario, an option with a $50 strike price would be completely useless.

Employee Stock Purchase Plans: A Way to Buy at a Discount

An Employee Stock Purchase Plan (ESPP) is a perk you'll typically find at publicly traded companies. It’s a program that lets you set aside a portion of your paycheck over time to buy company stock at a discount.

Here’s the typical flow:

- Enrollment: You decide to contribute a percentage of your after-tax pay, usually somewhere between 1% and 15%.

- Accumulation: The company collects these contributions over an "offering period," which is often six months long.

- Purchase: At the end of the period, all the money you’ve saved up is used to buy company shares for you.

The real magic is in the discount, which can be as high as 15% off the market price. Some of the best ESPPs even have a "lookback" feature. This means the discount is applied to the stock price from either the start of the offering period or the end of it—whichever is lower. This little feature can seriously amplify your returns, making ESPPs a fantastic and relatively low-stress way to build wealth as a shareholder.

How Vesting and Valuation Define Your Equity

Getting an equity grant feels like a major win, but it's really just the starting line. Two concepts turn that piece of paper into a real asset: vesting and valuation. If you don't get how these work, you won't know what your equity is actually worth or when you can truly call it your own.

Think of vesting as earning your equity over time. A company doesn't just hand over a valuable stake on day one. Instead, you gain ownership rights by sticking around and contributing to the company's growth.

Valuation, on the other hand, is all about putting a dollar figure on that ownership. This is simple for a public company but gets a lot more complicated for a private startup. Together, these two mechanisms determine the actual, real-world value of your equity package.

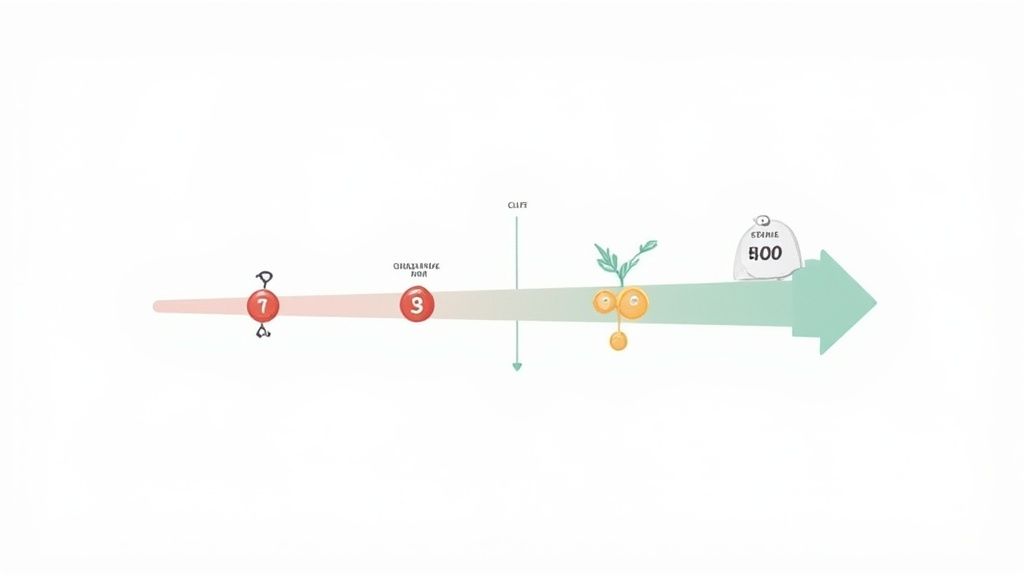

Understanding Vesting Schedules

A vesting schedule is the timeline that dictates when you get full ownership of your equity. It's basically a loyalty program. The longer you stay, the more of your grant becomes yours to keep, even if you eventually leave. This is precisely what makes equity such a powerful tool for keeping talented people on board.

The most common setup you'll run into is a four-year plan with a one-year "cliff."

- The Cliff: This is your first major milestone, and it's all or nothing. You typically have to work for one full year before you get your first chunk of equity—usually 25% of your total grant. If you leave before that first anniversary, you walk away with nothing.

- Graded Vesting: Once you're past the cliff, the rest of your equity starts to vest in smaller, regular increments. This usually happens monthly or quarterly for the next three years. For instance, after your one-year cliff, you might vest an additional 1/36th of the remaining shares every month.

Think of it like a video game. You have to complete the first level (the one-year cliff) to unlock your initial set of powers. After that, you earn new abilities gradually as you keep playing (monthly vesting).

Putting a Price on Your Shares

Okay, so you know when you'll own your shares. The next big question is: what are they actually worth? This is where valuation comes into play, and how it works depends heavily on whether your company is public or private. For marketers weighing job offers, this distinction is critical because it directly impacts how and when you can turn that equity into cash.

Your shares' value is a core part of what’s often called variable compensation, since its worth can change dramatically based on company performance.

For Public Companies This is the easy part. A public company’s stock trades on an exchange like the NASDAQ or NYSE. The value of a share is its current market price, which you can look up any time. It's transparent, liquid, and updated constantly.

For Private Companies (Startups) Here’s where it gets murky. With no public market, a private company has to figure out its own value. This is typically done through a formal process called a 409A valuation. An independent firm analyzes the company’s financials, market position, and growth potential to set a Fair Market Value (FMV) for its stock. This FMV is what sets the strike price for your stock options.

Key Valuation Terms to Know

When you look at your offer letter or grant documents, you'll see a few specific terms tied to value. Here are the ones you absolutely need to know:

- Strike Price (or Exercise Price): This only applies to stock options. It's the fixed, unchanging price you’ll pay per share to buy your stock when you decide to exercise.

- Fair Market Value (FMV): For private companies, this is the official per-share value determined by that 409A valuation. For public companies, it’s simply the current stock price.

- Total Grant Value: This is often shown as the number of shares you're granted multiplied by the current FMV. Just remember, this is a snapshot in time. The real value will go up or down as the company's valuation changes.

This practice of offering ownership isn't a niche perk; it's a global standard. A worldwide survey found that 97% of multinational companies offer some form of equity compensation. The most common type is service-based awards like RSUs, which shows just how much companies rely on vested ownership to retain top talent. You can learn more about these trends in the 2025 Global Equity Insights Survey.

Navigating the Tax Rules of Your Equity

Let's be honest: taxes are probably the most intimidating part of dealing with equity compensation. But you don’t need to be a tax lawyer to get the basics down. Understanding when and how your equity gets taxed is crucial for making smart financial moves and, more importantly, avoiding a nasty surprise from the IRS.

We’ll walk through the key moments that can trigger a tax bill, without getting bogged down in confusing jargon.

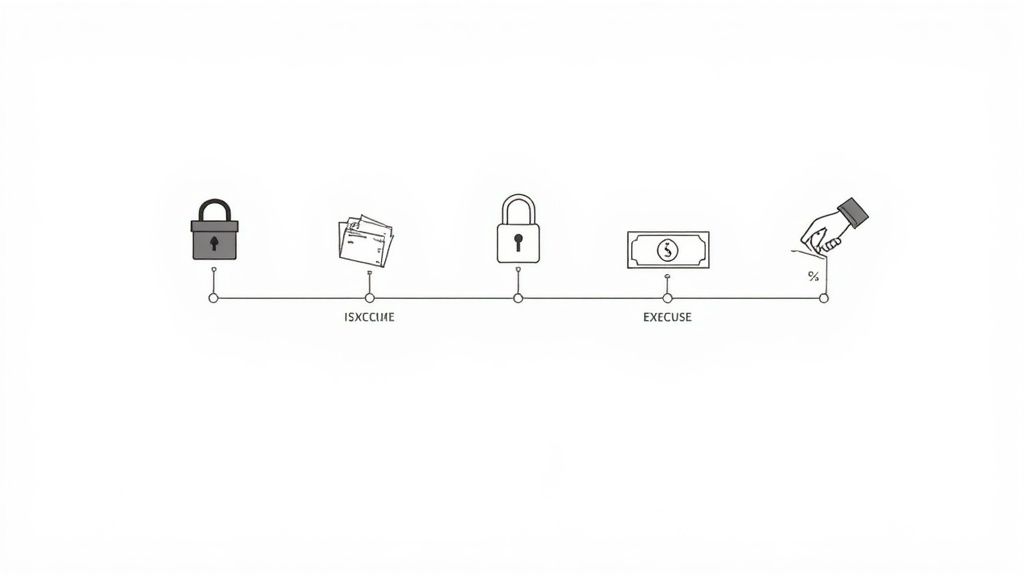

Think of your equity journey as having four potential milestones: the grant, vesting, exercise, and sale. Each one can be a taxable event, depending entirely on what kind of equity you have. Knowing what happens at each stage is the key to planning ahead.

When You Owe Taxes on Your Equity

The type of equity you hold—whether it’s RSUs or some flavor of stock options—completely changes the tax game. Let's break down what you can expect.

For Restricted Stock Units (RSUs)

With RSUs, things are pretty straightforward. The moment your RSUs vest, the IRS sees that as income. The total market value of those shares on that day is taxed as ordinary income, just like your regular paycheck.

Your employer usually handles this by withholding a portion of the shares to cover the taxes automatically. So, if 100 shares worth a total of $10,000 vest, your company might sell, say, 30 of those shares to pay federal and state taxes. You get to keep the remaining 70 shares.

For Stock Options (NSOs and ISOs)

This is where things get a bit more complex. The rules are very different for Non-qualified Stock Options (NSOs) versus Incentive Stock Options (ISOs).

- Non-qualified Stock Options (NSOs): When you exercise NSOs, the "bargain element"—that sweet gap between the market price and your lower strike price—is taxed as ordinary income.

- Incentive Stock Options (ISOs): ISOs are designed to give you a potential tax break. You generally don't owe ordinary income tax when you exercise them. But this is where the infamous Alternative Minimum Tax (AMT) can sneak up on you.

The AMT is basically a parallel tax system designed to make sure high-income folks pay at least a minimum amount of tax. The bargain element from exercising ISOs is a classic AMT trigger, and it can lead to a huge, unexpected tax bill if you aren't ready for it.

Capital Gains Tax When You Sell

Okay, so you’ve vested, exercised, and now you own the shares. The final tax event happens when you decide to sell. Any profit you make from that sale is hit with capital gains tax.

The rate you'll pay depends entirely on how long you held onto the shares:

- Short-Term Capital Gains: If you sell the stock within one year of acquiring it, your profit gets taxed at your higher ordinary income tax rate.

- Long-Term Capital Gains: Hold the stock for more than one year, and you qualify for the much friendlier long-term capital gains tax rate. This is a massive tax advantage.

Understanding this difference is fundamental. A little bit of patience can make a huge difference in how much cash ends up in your pocket.

A Simple Guide to Equity Tax Events

This table breaks down the critical moments when you might face taxes for different equity types, helping you anticipate your obligations.

| Equity Type | Taxed at Grant? | Taxed at Vesting? | Taxed at Exercise? | Taxed at Sale? |

|---|---|---|---|---|

| RSUs | No | Yes (Ordinary Income) | N/A | Yes (Capital Gains) |

| NSOs | No | No | Yes (Ordinary Income) | Yes (Capital Gains) |

| ISOs | No | No | Potentially (AMT) | Yes (Capital Gains) |

This framework is a great place to start, but keep in mind that tax laws are always in motion. Governments around the world frequently tweak policies to encourage employee ownership while managing tax revenues. For instance, recent updates in China and Germany have changed how equity income is handled, impacting countless employees at global companies. These international shifts really underscore why it's so important to stay informed. You can discover more insights about how global equity plans are managed on compensationstandards.com.

Ultimately, while this guide helps clarify what is equity compensation and how it's taxed, it’s no substitute for professional advice. You should always talk to a qualified financial advisor or tax pro to build a strategy that fits your unique situation. They can help you model different outcomes, plan for cash needs, and navigate tricky rules like the AMT.

How to Evaluate and Negotiate Your Equity Offer

An equity offer can feel like a lottery ticket—exciting, sure, but also incredibly abstract. To figure out what it's really worth, you have to look past the impressive number of shares and start asking the right questions. Evaluating your equity package isn’t about guesswork; it's about piecing together a few key data points to paint a clear financial picture.

https://www.youtube.com/embed/ERH212J5yqQ

This framework will help you turn a confusing jumble of numbers into a tangible asset you can discuss with confidence. The goal here isn't just to accept an offer. It’s to understand it, value it, and, if the situation calls for it, improve it.

The Essential Questions to Ask

Before you can run any numbers, you need information that almost never shows up in the initial offer letter. Getting these details is your first—and most critical—step. Don't be afraid to ask the hiring manager or recruiter for this info. It signals that you're a serious candidate who understands the value of equity.

Here’s what you need to find out:

- How many total shares are outstanding? This is the entire pool of shares the company has issued. Without it, your grant number is meaningless.

- What was the last 409A valuation? For a private company, this is a formal appraisal that sets the Fair Market Value (FMV) of a single share. This valuation determines the strike price for options.

- What type of equity is it? Are you getting ISOs, NSOs, or RSUs? As we’ve covered, they all have very different tax implications.

- Is there an early exercise policy? This allows you to purchase your stock options before they vest, which can offer a huge tax advantage down the road (though it comes with its own risks).

Once you have these answers, you can move from a vague sense of ownership to a concrete calculation of your potential stake.

Calculating Your Ownership Percentage

Being granted 10,000 options means absolutely nothing in a vacuum. Is that 10,000 out of a million total shares, or out of 100 million? Context is everything.

To figure out your piece of the pie, use this simple formula:

(Number of Shares in Your Grant / Total Number of Outstanding Shares) x 100 = Your Ownership Percentage

Let’s say you’re granted 20,000 shares and the company has 10,000,000 total shares outstanding. Your ownership stake is 0.2%. This percentage is your starting point for understanding the real-world value of your offer.

From there, you can estimate the current paper value. If the company’s latest 409A valuation priced a share at $5, your 20,000-share grant has a current theoretical value of $100,000. Just remember, this is a snapshot in time—the real value is in the company's future growth.

Smart Negotiation Strategies

Once you have a clear picture of what’s on the table, you can approach the negotiation strategically. While some parts of an equity offer are set in stone, others have more wiggle room than you might think.

What You Can Likely Negotiate:

- The Number of Shares: This is the most common lever to pull. If you bring competing offers to the table or can clearly demonstrate your high value, asking for a larger grant is a perfectly reasonable request.

- Vesting Schedule Acceleration: For more senior roles, you might be able to negotiate for accelerated vesting. This could trigger if the company is acquired or if you hit certain performance milestones.

What You Likely Can't Negotiate:

- The Strike Price: In a private company, the strike price for stock options is directly tied to the 409A valuation. Companies legally can't offer you a lower price, so this is almost always non-negotiable.

When you sit down to talk, frame your requests around your expected contribution and market value. Coming prepared with data and a solid understanding of the offer makes the conversation much more productive. For a deeper dive, our guide on how to skillfully counter a job offer provides a detailed roadmap for these important conversations. Your equity is a huge part of your total compensation, so give it the same serious attention you give your salary.

Common Questions About Equity Compensation

Even once you get the hang of what equity is, real-life situations always bring up more questions. Your grant agreement is always the final word, but knowing the answers to a few common "what-ifs" gives you a solid foundation for making smart career and financial moves.

Let's walk through some of the questions that almost everyone asks at some point. Getting these cleared up will help you feel more prepared for the key moments in your equity journey.

What Happens to My Equity If I Leave the Company?

This is probably the most critical question on the list. The short answer is: when you leave your job, any equity that has already vested is yours to keep. The unvested portion goes back into the company's equity pool for future employees.

But what "keeping it" actually means depends on what kind of equity you have:

- Vested RSUs: These are shares you already own, plain and simple. Once they're yours, you can hold or sell them based on company policy (and legal rules, if it's a public company).

- Vested Stock Options: Here, you don't own the shares yet—you own the right to buy them. When you leave, a countdown starts. You get a limited time, called a post-termination exercise period, to decide if you want to purchase your vested shares. This window can be as short as 90 days, so you have to move fast.

Always, always check your grant agreement for the exact rules. Some forward-thinking companies are starting to offer longer exercise periods, which can be a game-changer.

Should I Exercise My Stock Options Early?

This is a more advanced move. "Early exercising" means buying your stock options before they've even vested. It’s a high-risk, high-reward strategy that you typically only see at very early-stage startups where the stock price is incredibly low.

So, why would anyone do this? The main driver is a potential tax advantage. When you buy the shares early for pennies, you start the clock on long-term capital gains much sooner. If you hold that stock for over a year after exercising, any future profit could be taxed at a significantly lower rate.

The risk, however, is very real. You're spending your own cash on shares you might forfeit if you leave the company before they finish vesting. This is a complex financial decision with big tax implications, so it's absolutely one to discuss with a qualified financial advisor before pulling the trigger.

Thinking about dilution can feel backward at first. While your ownership percentage shrinks, the goal of a new funding round is to make the entire company pie so much larger that your smaller slice is worth far more than your original, bigger one.

What Is Dilution and How Does It Affect My Shares?

Dilution is a totally normal part of a growing company's journey. It happens whenever the company issues new shares of stock, usually to raise money from investors in a funding round. With more shares in existence, every existing shareholder’s piece of the pie gets a little smaller, percentage-wise.

Seeing your ownership percentage drop can be jarring, but it isn't automatically a bad thing. That new investment is supposed to rocket the company’s growth and increase its overall value. So, while your slice of the pie might be smaller, the hope is that the whole pie gets so much bigger that your slice is worth way more than before.

Can I Lose Money on My Stock Options?

Yes, it’s possible, but not in the way you might think. You only really risk the money you put in.

If your company's stock price drops below your strike price, your options are called "underwater." This means it would cost you more to buy a share than it's actually worth. In this case, your options are basically worthless unless the stock price bounces back. You haven't lost any of your own money, but the potential value of your grant has evaporated.

The only way you lose actual cash is if you exercise your options (paying the strike price) and then the stock’s value falls below what you paid for it, including any taxes you owed.

At SalaryGuide, we believe that understanding every piece of your compensation is the first step toward building a more rewarding career. Our platform gives marketing professionals the data-driven insights and tools to evaluate their total pay—equity included—and negotiate with real confidence. Take control of your career journey with SalaryGuide.com.