what is cost of living adjustment: how it can boost your pay

Ever heard the term "COLA" and wondered what it meant for your paycheck? Simply put, a cost-of-living adjustment (COLA) is an increase in your pay designed to help you keep up with inflation.

It's not a raise you get for crushing your sales goals or launching a killer campaign. Instead, it’s an adjustment meant to ensure that your salary's buying power doesn't shrink as the cost of everything from groceries to gas goes up. Think of it as your employer giving your paycheck an annual tune-up to keep pace with the economy.

Understanding the Purpose of a COLA

Here’s a simple analogy: imagine your salary is a boat tied to a dock. Inflation is the rising tide. Without a COLA, that rising water level—the increasing cost of goods—threatens to swamp your boat. A cost-of-living adjustment acts like a mechanism that raises the dock, keeping your financial boat safely above water.

The whole point is to maintain your standard of living, not to reward you for a job well done.

This is a really important distinction to make. A merit raise is all about recognizing your personal contributions and achievements. A COLA, on the other hand, is a much broader economic tool. It’s a direct response to the fact that $50,000 this year simply doesn't buy what it did last year. Without that adjustment, your real income actually goes down over time, even if the number on your paycheck stays the same.

For a quick reference, here’s a breakdown of the core concepts behind COLA.

| COLA at a Glance Key Concepts |

|---|

| Concept |

| Inflation Hedge |

| Not Performance-Based |

| Maintains Living Standard |

| Economic Adjustment |

This table helps put the fundamental purpose of a COLA into perspective—it’s about economic fairness and stability, not a reward system.

Who Receives a COLA

When people think of COLAs, they often picture government and public sector jobs. And for good reason. For decades, these adjustments have been a key tool for protecting the incomes of public servants and retirees.

In the United States, for example, the Social Security Administration has used an automatic COLA every year since 1975 to adjust benefits based on inflation. You can learn more about this long-standing practice and its history over at ADP.com.

But COLAs aren't just for government employees. Plenty of private companies offer them, too, particularly in a few common scenarios:

- Union Contracts: It's common for labor agreements to include clauses that guarantee an annual COLA.

- High-Cost Locations: Companies in major cities with sky-high living expenses often use COLAs to attract and keep top talent.

- Company Policy: Some organizations proactively build automatic COLAs into their compensation strategy to promote financial wellness among their staff.

A COLA is fundamentally about preservation. It preserves your purchasing power, employee morale, and a company's reputation as a fair employer in a constantly changing economic environment.

Of course, a COLA is just one piece of your financial puzzle. To really understand your earnings, you need to see how it fits with bonuses, benefits, and stock options. Our guide on what is a total compensation package breaks down how all these elements work together. Getting a handle on the bigger picture helps you see the true value your employer provides, well beyond your base salary.

How COLAs Are Calculated

Figuring out a cost-of-living adjustment isn't some mystical financial art; it really just boils down to tracking inflation with a specific tool. The go-to measure for this is the Consumer Price Index (CPI), which is published by the Bureau of Labor Statistics.

Think of the CPI as a giant, standardized shopping basket filled with all the goods and services a typical household buys. We're talking everything from groceries and gasoline to rent, doctor's visits, and even concert tickets. By tracking the total price of this basket from month to month and year to year, economists get a clear picture of how fast prices are rising.

So, if that basket of goods costs 3% more this year than it did last year, that tells us the inflation rate is 3%. That number often becomes the direct basis for the COLA percentage.

Different Flavors of the CPI

Now, it gets a little more nuanced. The government doesn't use a single, one-size-fits-all CPI. They actually track a few different versions tailored to specific groups of people, and the one that's used can change the final COLA number.

The two you'll hear about most often are:

- CPI-U (Consumer Price Index for All Urban Consumers): This is the big one, covering about 93% of the U.S. population. It tracks spending for pretty much everyone in urban areas—professionals, people who are self-employed, retirees, you name it.

- CPI-W (Consumer Price Index for Urban Wage Earners and Clerical Workers): This index is much more focused. It only looks at households that get most of their income from hourly wages or clerical jobs, representing about 29% of the population. This is the official index used to determine the annual COLA for Social Security benefits.

Why does the distinction matter? Because these groups spend their money differently. For example, the CPI-W might place a heavier emphasis on the cost of gas if wage earners spend a larger chunk of their budget on commuting. Those small differences can lead to slightly different inflation rates and, in turn, different COLA adjustments.

A Simple COLA Calculation Example

Let's put this into practice with a real-world salary. The formula itself is incredibly simple.

Current Salary x COLA Percentage = Salary Increase

Let's say you're a marketing manager earning $80,000 a year. Your company announces a COLA based on the latest CPI data, which shows a 2.8% rise in the cost of living.

Here’s how to do the math:

- Current Salary: $80,000

- COLA Percentage: 2.8% (or 0.028 in decimal form)

- The Math: $80,000 x 0.028 = $2,240

That $2,240 is the adjustment amount added to your pay for the year.

Your new salary becomes $82,240. It's important to remember this isn't a merit raise or a performance bonus. It's simply a practical adjustment to help your paycheck keep up with the rising cost of, well, everything.

Comparing COLA in Public and Private Sector Jobs

Ever hear the news about a big cost-of-living adjustment and wonder why your paycheck doesn’t reflect it? The answer often boils down to a simple but crucial difference: whether you work for the government or a private company. COLA isn't a one-size-fits-all deal, and where you work completely changes the game.

For public sector employees—think federal workers or Social Security recipients—COLAs are a pretty standard, predictable part of the equation. These adjustments are usually written into law to make sure that government wages and fixed incomes don't lose their buying power to inflation. It's an expected, almost automatic, update.

This infographic breaks down the basic process of how inflation data turns into a COLA.

As you can see, it's a direct line: consumer price data is collected, the percentage change is calculated, and that figure dictates the adjustment to someone's income. Simple as that.

Private Sector Discretion and Strategy

Now, step into the private sector, and the landscape shifts dramatically. For most companies, deciding to offer a COLA is entirely up to them. There's no law on the books forcing their hand, which turns the whole thing into a strategic business decision.

So, why would a company choose to offer a cost-of-living raise? It usually comes down to a few key motivators:

- Talent Retention: In a competitive job market, especially in pricey cities, a COLA can be the key to keeping great people from jumping ship for a better offer that actually covers their bills.

- Employee Morale: When inflation is high, everyone feels the squeeze. Acknowledging that financial pressure with a COLA can do wonders for morale and build serious loyalty.

- Contractual Obligations: Some private-sector employees do have a guaranteed COLA, but it's typically because it was negotiated into a union contract or collective bargaining agreement.

The core difference is simple: in the public sector, a COLA is often a matter of policy and law. In the private sector, it's a strategic business decision balancing budgets, competition, and employee well-being.

The mechanics are worlds apart. In the U.S., the Social Security COLA is set by federal statute, but at a private company, the terms are dictated by internal policy or labor contracts. During the high-inflation crunch of 2022 and 2023, some forward-thinking U.S. employers gave out COLAs topping 8% just to help their teams keep up. You can find more COLA adjustments insights at People Managing People.

This contrast is exactly why the national COLA figures you see on the news rarely match what’s happening in your office. While public adjustments are a direct reaction to economic data, private ones are a reaction to business needs. Understanding that distinction is the first step to setting realistic expectations for your own salary.

Using Geographic COLA for Relocation and Remote Work

As work gets more flexible, where you plug in your laptop has a massive impact on your paycheck. This is where a geographic cost of living adjustment comes into play. Often called a "geo-differential," it's how companies fine-tune salaries when employees move between cities with wildly different expenses.

This isn’t about annual inflation. It’s about the here-and-now cost differences between one place and another.

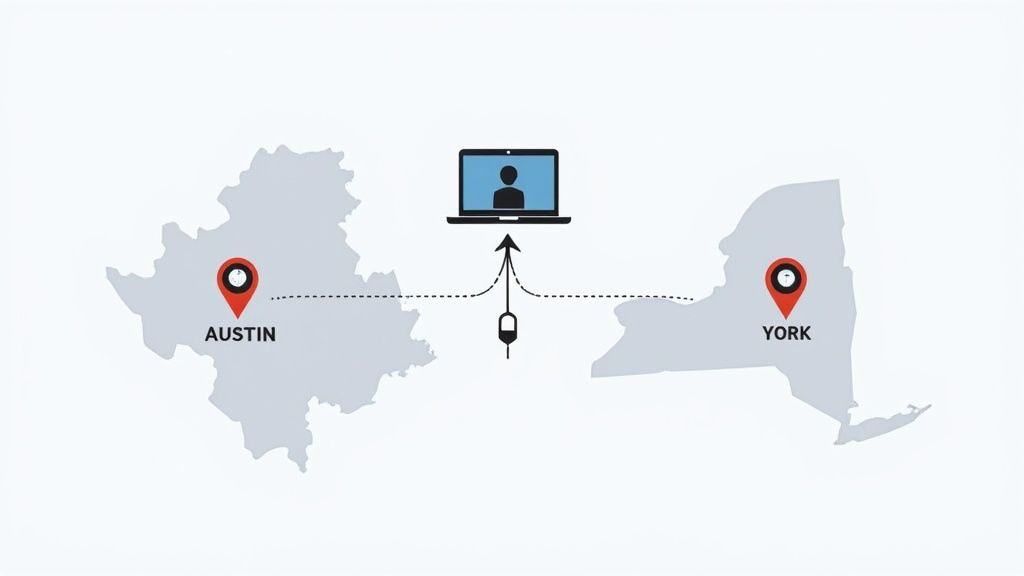

Think of it this way: a marketer earning $100,000 a year in Austin, Texas, gets the chance to transfer to the company's New York City office. Since the cost of pretty much everything is higher in NYC, the company will likely offer a positive COLA. This pay bump ensures the employee's purchasing power doesn't take a nosedive.

The reverse is also true. If someone moves from a high-cost hub like San Francisco to a more affordable city like Omaha, their salary might be adjusted downward. While no one likes seeing their base pay decrease, the goal is to maintain an equivalent standard of living in the new, cheaper location.

Navigating Remote Work Compensation Models

The explosion of remote work has thrown a wrench into traditional pay structures. Companies are still experimenting with the best way to handle compensation when employees are scattered across the country, but a few common models have taken shape.

Headquarters-Based Pay: Some employers, especially those in pricey tech hubs, pay everyone based on the high cost of living at their HQ. It's a great recruiting tool but can lead to big pay disparities among colleagues doing the same job from different cities.

Location-Based Pay: This is the most popular approach. An employee's salary is tied to the cost of living and local market rates where they actually live. Your paycheck reflects the economic realities of your hometown.

National Standard Pay: A less common but growing trend is to set a single salary band for each role, no matter where the employee is located. This method puts the focus squarely on the value of the job itself.

A geographic cost of living adjustment ensures that an employee's salary provides a consistent lifestyle, whether they are in Manhattan or a small town in the Midwest. It’s about maintaining purchasing power parity across different economic landscapes.

This idea goes global, too. For international assignments, these adjustments are non-negotiable. The cost differences between countries can have a huge effect on an employee's disposable income, so multinational companies use COLA to ensure their expatriate staff can maintain a lifestyle comparable to what they had back home. You can learn more about how COLAs support global mobility on eca-international.com.

Whether you’re eyeing a relocation or settling into a remote role, it's crucial to understand your company's philosophy on geographic pay. Modern career tools can give you the data you need to have an informed conversation. You can explore how SalaryGuide integrates COLA insights to see how these platforms make complex pay calculations more transparent for everyone.

How a COLA Impacts More Than Just Your Paycheck

A cost-of-living adjustment feels great on payday, but its effects don't stop there. This bump in pay sends ripples through your entire financial picture, from taxes to long-term savings. While the extra cash in your pocket is the main event, it's smart to understand the other moving parts.

First up, taxes. Since a COLA is treated as regular income, it can sometimes push you into a higher tax bracket. This is a classic case of "bracket creep," where a larger chunk of your earnings gets withheld, which can slightly reduce the net gain from your raise. It’s something to be aware of so you aren't surprised when you look at your pay stub.

A Welcome Boost to Your Benefits and Retirement

Now for the good news. A higher base salary from a cost-of-living adjustment can seriously amplify your workplace benefits. Many of the best perks are tied directly to your annual pay, so when your salary goes up, their value does too.

Think of it as a positive chain reaction that touches several key areas:

- 401(k) Contributions: Let's say your company matches 50% of your contributions up to 6% of your salary. A higher salary means a bigger dollar-for-dollar match from your employer, turbocharging your retirement savings.

- Life Insurance Coverage: Company-provided life insurance is often set as a multiple of your salary—say, one or two times your annual pay. A COLA automatically increases the value of this safety net for your family.

- Disability Insurance: Benefits for both short-term and long-term disability are calculated as a percentage of your income. A bigger salary ensures you have better income protection when you need it most.

A COLA isn't just about keeping up with today's expenses; it's an investment in your future. By lifting your base salary, it strengthens your retirement accounts and insurance coverage without you having to lift a finger.

After getting a COLA, it's the perfect time for a quick financial check-up. Make sure your 401(k) contribution percentage is still high enough to capture the full company match on your new, higher salary. This simple review ensures you're squeezing every bit of value from your pay adjustment, helping you build a more secure financial future.

How to Talk About a COLA With Your Boss

Talking about money is never easy. But when it comes to a cost-of-living adjustment, the conversation doesn't have to be intimidating. The secret is to approach it as a business discussion based on economic data, not as a personal plea for more cash.

Start by doing your homework. You need to build a case that’s grounded in facts, not just feelings. Find official data showing exactly how inflation is hitting your local area.

This simple act of preparation transforms a potentially awkward request into a productive conversation. You're not asking for a raise, you're discussing how to keep your compensation fair and competitive in a changing market.

Build Your Case with Solid Data

The go-to source for U.S. inflation data is the Bureau of Labor Statistics (BLS). They regularly publish updates on the Consumer Price Index (CPI), which is the gold standard for measuring inflation. Make your argument even stronger by finding the specific CPI data for your city or metropolitan area.

When you sit down with your manager, present the information calmly and professionally. You could say something like this:

"I’ve been keeping an eye on the local CPI data, and it shows the cost of living in our city has jumped significantly this past year. I'd like to talk about how my compensation can be adjusted to reflect that, so my pay keeps its real-world value."

This kind of opener immediately shows you’re an informed, thoughtful employee. It proves you're not just asking for a random bump in pay but are thinking critically about your salary in the larger economic picture.

Frame the Conversation for a Win

It’s crucial to remember this isn’t the same thing as asking for a raise based on your performance. While the two can be related, a COLA discussion should stay focused on the hard economic numbers.

Here are a few tips to steer the conversation in the right direction:

- Make it About Retention: Frame your request around mutual benefits. Explain that an adjustment helps you stay focused and committed to your job, free from the financial stress that inflation can cause. It’s an investment in keeping a good employee.

- Be a Collaborator: Treat it like a problem-solving session, not a demand. Ask about the company's official policy on inflation adjustments and how they're handling compensation in the current economy.

- Know Your Number, But Be Flexible: Have a clear idea of what you’re asking for. At the same time, be open to discussion. The company might have its own way of calculating these adjustments or other benefits to offer.

For a deeper dive into salary negotiation tactics, check out our complete guide on asking for a raise. It gives you a step-by-step playbook to help you prepare for this important conversation.

Answering Your Top Questions About COLA

As you get a better handle on the what, why, and how of cost-of-living adjustments, a few practical questions naturally start popping up. Let’s tackle some of the most common ones to give you a complete picture of how COLA works in the real world.

One of the first things people wonder is whether employers are actually required to offer a COLA. The short answer is no, at least not for most private-sector jobs. Unless it's specifically written into a union contract or an individual employment agreement, there's no federal or state law that forces companies to provide these adjustments. It’s almost always a discretionary choice.

Distinctions and Timelines

It's also easy to mix up a COLA with a merit raise, but they serve two totally different purposes. A COLA is all about reacting to external economic shifts—namely inflation—to help your salary keep its purchasing power. A merit raise, on the other hand, is a reward for you—your performance, your contributions, and your growth at the company.

Think of it this way: A COLA keeps you at the starting line financially, while a merit raise moves you forward on the track. One is about staying even with the economy; the other is about getting ahead because of what you've achieved.

So, how often can you expect these adjustments? For companies that do offer them, COLAs are typically handed out annually. This timing makes sense, as it lines up with the release of yearly inflation data, letting employers make one consistent adjustment for everyone. This annual cycle helps create clear and predictable expectations for the whole team.

Finally, here’s a curly one: can a cost-of-living adjustment ever be negative? While it's incredibly rare, it’s technically possible. This would only happen during a period of deflation, where the overall cost of goods and services actually goes down. If the CPI turned negative, a COLA could theoretically result in a pay cut. In reality, most employers would avoid this at all costs to prevent a massive morale hit, making it more of a theoretical curiosity than a common practice.

Ready to see how your salary stacks up in today's market? SalaryGuide provides real-time compensation data and career intelligence specifically for marketing professionals. Get the insights you need to understand your worth and negotiate with confidence.